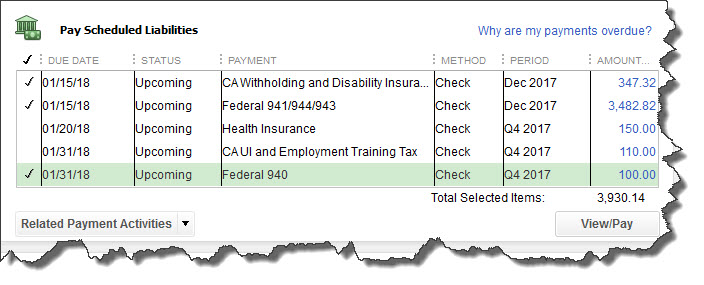

Accounts Payable (A/P). Everything that you owe to vendors, contractors, consultants, etc. is tracked in this account.

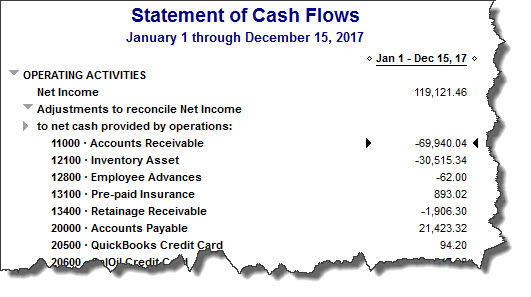

Accounts Receivable (A/R). This account tracks income that hasn’t been realized yet, like outstanding invoices.

Accrual Basis. This is one of two basic accounting methods. Using it, you record income as it is invoiced, not when it’s actually received, and you records expenses like bills when you receive them. Using the other method, Cash Basis, you would report income when you receive it and expenses when you pay the bills.

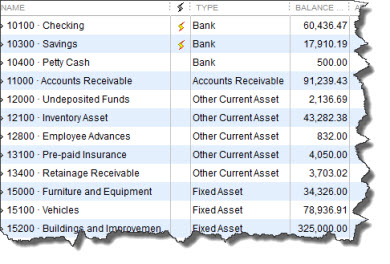

Asset. What physical items do you own that have value? This could be cash, office equipment and real estate. In QuickBooks you’ll be managing two types. Current Assets are generally used within 12 months (or you could convert them to cash in that length of time). Fixed Assets refers to belongings like vehicles, furniture and land, property that you probably won’t use up in a year and which usually depreciates in value. Depreciation is very complex; you may need our help with that.

Average Cost. This is the inventory costing method that programs like QuickBooks Pro and Premier use to calculate the value of your stock.